Global Markets

US Yield Curve & Fed Rate

Monitor

Crypto Market Tracker

Key Macro & Technicals

Market Commentary

·

MSCI World and

S&P 500 continues to extend the up-move having rallied 4.4% and 5.4% around

the last 2 weeks. Mag 7 clearly outperforming as NASDAQ moved even higher +7.2%

in the same period. ROW equities also positive by not much between 0.4$ - 1.6%

except for Russia Index which pulled back 1.9%. Deeper dive reveals that

S&P 500 has gapped through key line of polarity 5780 and broken above

200-day SMA recently despite the weak trading volume but rising market breadth.

In the 09/24 publication, we had forecasted S&P 500 hitting 6100 levels

which came to passed and after that next level 7200 – 7363. Updated the Fibo

clusters and there is an interim level 6840 – 6915 and reconfirmed 7212 – 7299

levels.

·

Having said that, still feel these higher levels are too high

given that 6100 level already +76% PnL from last COVID low 3500 in FY2020. Based

on S&P 500 trading history since GFC 2008, the index has rallied 34 – 120%

each trading cycle so 76% PnL from 10/22 low is getting towards the high end of

the range. Also, Fibo time projection indicate that 23 – 29 May is an important

week so we need to keep close watch for any reversal sign. In terms of trading

intuition, would feel that next Fibo level 6450 would be a more realistic ATH

so the remaining 20% equity position being kept for that purpose. Also, noticed

harami cross forming on 19/05 and the index has pulled back from 5970 to 5844

since then.

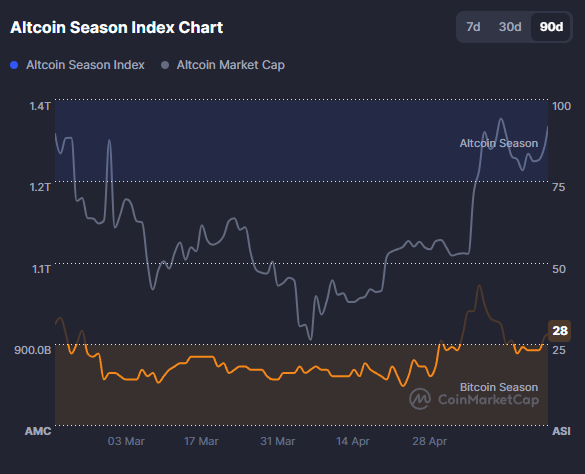

· FX markets been lackluster with USD Index only down -0.8%. Both G7 and Asian currencies have hardly moved with even the volatile AUD/JPY only dropping 1.6%. DEER model showing that JPY and CNY are the most undervalued versus the USD. Same goes for fixed income, REIT and commodities with 10Y UST +0.9%, IYR + 1.3% and GPSCI +0.3%. Even crypto has hardly moved but noticed BTC/$ settling into $109k level quite well this week. Only exception is BNB/$ retracing 12%.

·

On 14/05, HSBC

expects $/MYR to reach 4.9 due to heightened uncertainty in the global economic

environment triggering GLC to repatriate more funds back to Malaysia to support

the Ringgit. “Total annual outbound portfolio investment jumped from $7B in 2022

to $10B in 2023 and then further moved to $24B in 2024. This makes Malaysia’s

portfolio outflows the fastest-growing in the region compared to historical

norms.

·

On17/05, the Fed

was noted to have quietly vacuuming up $43.6B in US Treasury with $8.8B in 30Y

bonds on 08/05 alone plus another $34.8B the week earlier. This monetary easing

has helped prop up BTC/$ prices, gold and Latam equities among other risk

assets.

·

On 13/05, China

cast itself as defender of the multi-lateral world order wooing Latin American

and Caribbean leaders at the China-CELAC Forum citing that “bullying and

hegemony will only lead to self-isolation”. Two-thirds of the countries have

signed up to the BRI infrastructure drive and China has surpassed the US as the

biggest trading partner of Brazil and Chile. Xi’s top diplomat also urged Latin

American nations to “join hands” with China to defend their rights against a

country that is “using tariffs as a weapon to bully other countries”

·

On 14/05, the UK

govt hit back as suggestions that the tariff agreement it reached with US last

week could be damaging to China. This was triggered by conditions requiring the

UK to “promptly meet” US demands on the “security of supply chains” of steel

and aluminum products exported to the USA. China is UK’s 5th

biggest trading partner and Beijing fears this arrangement could evolve into

being excluded from supplying US-bound goods to the UK stating it was a basic

principle that bilateral trade deals should not target other countries

·

On 15/05, US

envoys in Africa will be rated on commercial deals struck, not aid spent

touring it as a new strategy for US support shifting the strategy to “trade, not

aid”. US ambassadors in Africa have already shepherded 33 agreements worth $6B

in Trump first 100 days. However despite Trump’s aggressive spending cuts,

Washington has pledged a $550M loan for the Lobita rail corridor, a shortcut

for copper and cobalt from Zambia and Congo to Angola’s Atlantic port bypassing

China-controlled routes. The US is keen to counter both Chinese and Russian

influence in the continent particularly over minerals and trade. In one of

China’s latest deals., a $652M loan agreement was agreed with Nigeria through

Exim bank for a highway feeding the new Lekki port and Dangote refinery.

·

On 19/05,

Treasury Secretary Scott Bessent said ratings were a “lagging indicator” and he

added that he believes “that’s what everyone thinks” of the grades from credit

agencies like Moody. This move has been long coming as Fitch made a similar downgrade

in 20223 and S&P as far back as 2011. The agencies highlighted the growing

US deficit now unusually high for a full-employment, peacetime economy as a key

justification. Moody has maintained a perfect rating on US debt since 1917.,

making the downgrade historically significant. China has also weighted in

urging the US to take responsible policy measures to maintain the stability of

the international financial and economic system and safeguard the interest of

investors

·

On 19/05, Japan

PM Shigeru Ishiba has rejected rolling out tax cuts funded by additional debt

as he argued that Japan financial situation worse than Greece. The backdrop for

Ishiba has been the prospect of declining support ahead of a key upper house

election in July with calls to slash taxes, including a levy on consumption and

increased spending. However, Japan status a foreign creditor and domestic

holding of sovereign debt has helped it evade the type of deep fiscal ructions

experienced by Greece in 2009.

·

On 09/05, Trump

did the trade deal with the UK with markets reacting well by rallying upon this

development. However, on closer inspection its still early days and a

nothingburger as UK constitutes only 3%

of all US trade whilst China is US’ 3rd largest trading

partner. In the UK deal, Bentleys which were to be taxed 27.5% are now only hit

with 10% tariff, British companies can now send plane part without tariffs and

same goes for steel, aluminum and beef. These are scant details and RSM Chief

Economist Joe Brusueles said “a trade agreement where details are still being

negotiated is not an agreement”.

·

On 08/05, there

were concerns that iron ore which is the major commodity most exposed to China

would be taking a hit on Trade War 2.0 but surprisingly the prices have been

resilient. China buys more than 70% of all seaborne volume which it uses to

produce just over 50% of global steel. This dichotomy is most likely due to the

fact that China’s steel demand is in sector less exposed to trade namely property

and infrastructure which accounts for 60% of total demand. Whilst property

sector has struggled in recent years, there are early signs that Beijing’s

stimulus efforts have stabilized the market. The trade-exposed part of steel

demand includes machinery, automotives and household appliances which together

constitute almost a third of consumption.

·

On 07/05, Eurizon

SLJ Capital’s Jen and Joana Frire wrote that the USD might face a $2.5T selling

avalanche as Asian countries unwind their stockpiles to protect themselves from

a deepening US-lead trade war. Jen also previously said that $1T could flow

back to China as Chinese companies sell their USD-denominated assets when the

Fed cuts interest rates. Accelerating this outflow might be “naked long-dollar

positions” prevalent amongst Asian countries that run large surpluses such as

Taiwan, Malaysia and Vietnam.

·

On 12/05, US and

China have agreed to 90-day pause and will each lower reciprocal levies

according to US Treasury Secretary Scott Bessent. BTC/$ has broken above $100k

mark with other risk assets and XAU/$ fell 1% on this recent development. Trump

has also signed an executive order to slaash US prescription drug prices by 30%

to 80% to align them with the lowest price paid globally.

·

On 11/05, Nifty 50

jumped +3% as a US-brokered ceasefire in the Kashmir region appeared to be

holding after India stuck several targets in Pakistan. However, Trump’s offer

to help broker a deal over the hotly contested Kashmir region appears to have

ruffled some feathers in New Delhi which historically remained skeptical of 3rd

party negotiations in the region.

·

On 09/05, Trump

surprisingly is pushing for a 39.6% tax rate on individuals earnings +$2.5M and

couples earning +$5M to help fund his economic package. The plan could raise

$67.3B over 10 yrs with additional $6.7B from eliminating the carried interest

loophole. The proposal aims to offset the costs of extending Trump’s 2017 tax

cuts but final agreement still pending.

·

On 08/05, GS

maintained its 12M US recession probability at 45% noting its not unusual for

hard data to lag event-driven recessions. Lower oil prices are positive for

Asian economies which if sustained will improve their current account balance

and act as a disinflationary force, providing more room for rate cuts. Also, GS

noted that xxx that retail investors bought the last dip, in line with previous

periods of major volatility.

·

On 07/05, Paul

Tudor Jones was on CNBC saying stocks are bound to hit new lows even if Trump

tones down his aggressive China tariffs.

·

On 07/05,

European equities declined on concerns that Germany’s Friedrich Merz will come

into power with diminished authority to push forward his agenda. Whilst Merz

secured parliamentary backing as Germany’s new chancellor after a 2nd

vote, the setbacks have reduced optimism for investors who were counting on

ambitious plans for defense and infrastructure spending. On the tariffs front

the EU plans to hit EUR 100B in US goods with additional tariffs in the event

ongoing trade talks fail to yield satisfactory results for the bloc.

·

On 07/05, LGT

Bank noted that current SPX record high in ROE 21.1% ranks in the 99th

percentile since 1975. Also, USD is overvalued by 16% with JPY and CNY being

the most undervalued.

·

The US trade

deficit has worsened during Trump tenure widening to $140.5B in 03/25 driven

by significant irse in imports of consumer good, autos and capital goods. Good

imports surged 30% y/y with industrial supplies +335% and consumer good +58%.

High-frequency data indicates that this import surge particular from the EU and

trans-shipment hubs like Vietnam and Thailand peak in mid-April and expected to

decline in May. This frontrunning activity, likely in anticipation of potential

trade disruptions suggest upcoming trade data will show notable drop in import

volumes.

No comments:

Post a Comment