Global Markets

US Yield Curve & Fed Rate

Monitor

Crypto Market Tracker

Key Macro & Technicals

Market Commentary

·

FX markets still

trading in a range last 1M with USD Index -0.3%. Big trend still dollar

weakness and stable $/CHF ironically the biggest movers during this period with

-1.8% move among the major currencies. Deeper dive, shows $/CHF following

through on the down-move since 2019 and next target would be ATL 0.7579 in

08/11. FX crosses also risk-on with EUR/JPY and AUD/JPY both rallying 3.5% and

3.8% respectively.

·

On 10/07, Well

Fargo strategists cited that the US economy appear to be losing steam with real

GDP contracting 0.5% in the 1Q25, a dip partly reflecting a surge in imports sparked

by businesses racing to lock in order before Trump’s elevated tariffs. All else

being equal, imports in national income and product accounts can mechnically

reduce GDP. They also added that their projection for real GDP expansion of

1.8% in the 2Q25 “may overstate the strength of the economy at present”.

·

On 29/06, China

manufacturing PMI fell abruptly to 49.7 as local manufacturers grappled with

sluggish overseas demand amid relatively high US trade tariffs. Washington and

Beijing were also seen agreeing to uphold the May deal, as well as establish a

framework for a trade deal in Jun 2025.

·

On 20/06, the USD

slipped to multi-year lows against EUR and CHF alongside Asia FX as concerns

about Fed independence undermined faith in the soundness of USA’s monetary

policy. InTouch Capital Markets Kieren said “market will likely bristle at any

early move to name Powell’s sucessor, particualrly if it appears

politically-motivated”. The ending of “US exceptionalism” has been a major

theme in the USD decline in recent months as investors question it dominant

reserve currency status and main safe haven among currencies

·

On 20/06, Chinese

Premier Li Keqiang said “China will take forceful steps to boost consumption”

at the latest AIIB annual meeting. Beijing has through late-2024 rolled out a

slew of measures aimed at boosting laggard consumer spending, most notably

subsidies on eletronics and household goods. Whilst the swathe of recent

econommic readings show some pressure from the US tarriffs, they also

highlighted the resilience of the Chinese economy

·

On 30/06, Canada

announced it would rescind its Digital Services Tax (DST) clearing the way for

the resumption of trade and security negotiations with the US, with both sides

aiming to strike a deal by 21/07. The decisions comes just days after Trump

abruptly called off trade talks on 28/06, denouncing the attack as a “blatant

attack”.

·

Most of the

action lie in MSCI World +3.7% and US equities as S&P 500, DJI, NASDAQ have

gained 4.7%, 5.2% and 6.1% respectively. Updated the FIbo projections and xxx

and 6500 levels now look within range for both MSCI World and S&P 500.

Another major mover has been the Nikkei 225 which has rallied +6% lately, which

has broken out a bullish triangle formation. CSI 300 bullish falling wedge

formation breakout also following as it been clinging to key 4000 level last

few months. Indian and Russian equities also experience positive momentum with

SENSEX, Nifty 50 and Russian Index jumping 3.1 – 3.5% range. Sector-wise most

of the gains have been around financials, technology and communication sectors

based on XLC, XLF, XLK with the only outlier being energy with XLE -3.8% no

doubt to to collapsing oil prices. Unsurprisingly, OVX has shot up 17.6% whilst

all other volatility indices like VIX, SKEW, VVIX have faded 20%.

·

Was reviewing

prior S&P 500 Fibo price targets which stood at 6120 – 6370 and 6940 in

09/24 as well as 6166 and 6465 in 11/24. Updating the Fibo clusters revael that

we are nearing the revised targets 6330 and 6487 levels. After that is 7160

which feels too aggressive from last low 3500 in 08/20 for this trading cycle.

·

On 26/06, market

chatter is that big investors are safeguarding against thinly-traded markets

given complacent market mood which might spark a repeat of Aug 2024 rout. They

see stocks, bonds and currencies vulnerable against the backdrop of fragile

Israel-Iran ceasefire, seesawing oil prices and trade-war uncertainty. HSBC

Asset Managment CIO Xavier said “our positioning is that over the next 3M

market will not get the positive confirmations they are pricing-in”.

·

On 30/06, GS

noted that US pension funds sold $28B in equities for their Jun rebalancing

following the S&P 500 hitting a new ATH. This selling amount ranks in the

89th percentile among all buy-and-sell estimates in absolute dollar

value last 3Y. Looking at longer timeframes, it also sits at 90th

percentile of similar transactions dating back 01/20.

·

On 09/07, most

Fed members eye rate cuts for 2H25 with divisions emerging on the exact path.

Some members feel a cut in Jul 2025 would make sense whilst others like Fed

Powell continue to back the wait-and-see approach citing uncertainty around

policy impacts from Washington on the economy and inflation. For 2026, the

voting Fed memebrs projected rates to fall to 3.6% in 2026, up from prior

forecast of 3.4% in 03/25. For 2027, the committee revised its policy rate

outlook higher, seeing rates falling to 3.4%, up from 3.1% previously. Macro

wise, inflation in both US and China are non-issues, US inflation continues to

fall despite Liberation Day and Chinese inflation remains in the negative

territory. This clearly strengthens the case for further Fed rate cut and PBOC

fiscal and monetary stimulus.

·

On 25/06, Trump

touted he might expediate his accouncement of the Fed Jerome Powell’s successor

according to a WSJ report. He has toeyd with the idea of selecting and

announcing the replacement by Sep/ Oct 2025 and considering former Fed governor

Kevin Warsha nd National Economic Council Director Kevin Hassett. Other

contenders include Treasury Secretary Scott Bessent, former World Bank

President David Malpass and Fed governor Christopher Waller. Fed Powell has

largely disregarded calls to cut rates immediately and has signalled he will

serve the remainder of his term which end May 2026.

·

On 29/06, Trump

has said he wants to to cut the Fed rate to 1% from 4.25 – 4.5% right now.

Investors are also keeping an eye on his massive tax cut and spending bill now

facing the Senate, which could add $3.3T to the national debt over a decade

according to the Congressional Budget Office estimates. This estimate hit to

the $36.2T federal debt is about $800B more than the version passed last month

in the House of Representatives. Democrats are hoping the latest revised figure

could stroke enough anxiety among fiscally-minded conversatives to persuade

them to buck the Republican party which controls both chambers of Congress.

·

“Republicans are

doing something the Senate has never, never done before, deploying fake maths

and accounting gimmicks to hide the true cost of the bill. They are about to

pass the sigle most expensive bill in US history to give tax breaks to

billionaires whilst taking away Medicaid, SNAP benefits and good paying jobs

for millions of people”, Democractic Senate Minority Leader Chuck Schumer said

as the debate opened on 29/06. Senate Republicans who reject the CBO’s

estimates on the legislation costs are set on using an alternative calculation

method that doest not factor in costs from extending the 2017 tax cuts. Using

this methodm the budget bill appears to cost substantially less and seems to

save $500B accroding to Bipartisan Policy Center and therefore a “magic trick”.

If the Senate passes the bill, it will then return to the House of

Representatives for the final passage before Trump can sign it into law.

·

On 25/06, UBS

said the tech rally has more legs as AI adoption spread across industries

likely crossing the 10% threshold, a milestone that took e-commerce +20 years

to achieve. Examples include Microsoft using AI for 30% of its coding worka and

PayPal handling 80% of customer support through AI tools. UBS expects global

capital spending to rise 33% in 2026 to $480B after surging 60% this year.

NVIDIA has surged to ATH $154.31 on 25/06 after an exceptionally bullish note

from Loop Capital triggered investor enthuisiam.

·

Fixed markets

been slow as well with 10Y UST bearish rising wedge breakout in 06/25 still in

play, targeting 3.88% levels is doable consdering we are entering 2H25 so Fed

has to make good on their forecasted cuts to avoid losing credibility. LQD,

HYG, EMB moved up slightly circa 0.3 – 0.9% so seems credit markets in a

holding pattern for now.

·

US REIT are stuck

too with IYR only -0.5% last 1M except for VNO has dropped 4.4% lately. S-REIT

and M-REIT however more buoyant with MAPL +3.6% and IGRE +13.2% which is pretty

significant. On deeper dive, IGRE is on a bull run hitting ATH and technicals

indicates there might be more to this recent upmove

·

On 25/06, DLR which

is a $59B market-cap REIT announced it will raising EUR 850M at 3.875% through

its subsidiary Digital Dutch Finco BV. The indenture govering the notes include

covenants restricting the company’s ability to incur additional indebtness and

requires maintainence of a pool of unencumbrered assets. The notes are

redeemable in whole or in part at the issuer’s option at 100% and make-whole

premium except within 90 days of maturity.

·

Broad commodities

still in doldrums with S&P GSCI -3% and Baltic Dry Index -15.5%. However,

there is some action in XPD/$ +18.3% and XPT/$ + 14% with oil and corn futures

dropping 6.2% and 7.3% respectively. Deeper dive into XPT/$ reveals it has

entered a big bull market lately jumping form $970 in 03/25 to $1402 today

which is a +40% price increase and a new ATH $1422 too. Corn futures at $400

now targeting low $360 on 08/24 and after that $301 on 04/20. The grain has

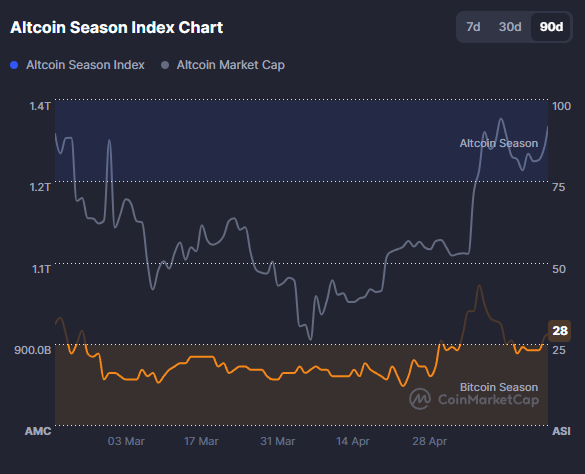

been on a massive downtrend last 3Y. BTC/$ made a new high at $119.5k with

SOL/$ and XRP/$ up 11.6% and 29.3% whilst

memecoins SHIB/$ and DOGE/$ also up 10.2% and 12.8% last 1M. On 09/07, US

copper imports also been hit by 50% tariffs to boost domestic production which

has disadvantaged big exporters Chile, Canada and Peru.

·

On 30/06, BTC/$

has hit $108k with the biggest driver was the progress of a stablecoin

regulation bills through Congress, highlighteing Trump’s commitment to doling

out more crypto-friendly regulations. Further signs of government adoption

continued with Freddie Mac and Fannie Mae signalling they would consider using

crypto as collateral in home loans. In addition to institutional adoption, risk

appetite was boosted over the past week by Israel and Iran ceasefire which

appears to be holding. According to Macquarie, Trump also seemed to dissuade

“regime change” in Iran, thus disminishing the prospect that Iran will devolve

into social instability or chaos. Also, the combination of Iran’s proportional

response and prospect that she will not disrupt the flow of oil has led of

large declines in the price of Brent crude.

·

As the 09/07

deadline for US-EU tariff deal approaches, with scant progress so far towards

mutually-agreed baseline levies, concern is growing over how long will market

stay numb to trade risks. Oil has swung $63 – 81/bbl in Jun making it once of

the most volatile months for crude in 15 years

·

On 25/06, oil

rises as draw in US crude stocks signal firm demand with de-escalation of

conflict between Iran and Israel refocusing market back to fundamentals. Oil

crude oil inventories fell for a 5th straight week whilst gasoline

stocks upexpectedly fell 2.1M barrels compared with forecase for a 318k barrel

build. On Saturday, Rosneft Igor Sechin said OPEC+ could bring forward it

output hike by around a year from initial plan. Meanwhile, Trump has hailed a

swift end to war between Iran and Israel and said Washington would likely seek

a commitment from Tehran to end its nuclear ambitions at the next talks.

Key QnA

·

xx