Global

Markets

US Yield Curve & Fed Rate Monitor

Crypto Market Tracker

Key Macro & Technicals

Market Commentary

· FX markets

continuing with USD weakness with Dollar Index -2.3% since 23/04. Key mover was

TWD which gained 11.2% apparently on FDI inflows and improvement in equity

sentiments. There is even a gap in the chart which has since been filled. Other

gainers have been AUD/$ and NZD/$ which both appreciated 4.7% whilst KRW and

MYR havew rallied 5.8% and 5.6% respectively

·

On 02/05,

Eurozone manufacturing PMI sees fastest growth in 3Y from low 43 in 06/23 to

reach 49 on 04/25 which is significant. On 01/05, BoJ cut its economic growth

forecast by ½ for 2025 to 0.5%, which is another piece of evidence that Trump’s

escalating trade war with friends and foes is hurting the global economy. It

also cut its growth forecast for 2026 to 0.7% from 1% prior projection. China

also reported that its factory activity contracted in April at the fatest pace

in 16M whilst IMF warned that global trade war will stymie growht particularly

in the US.

·

On 05/05, Ed

Yardeni lowered the probability of a US recession to 35%, reversing a March

increase to 45% as he belives China and US both may be ready to suspend their

tariffs while they negotiate a trade deal. Yardeni also cited political

considerations are Trump may be motivated to resolve trade tensions ahead of

midterm elections to help Repulicans preserve their congressional majorities.

·

On 04/05, US

unemployment rate increased to 4.2% from 3.4% in 2023 and layoffs jumped +60%

in April to +105k according to Chalelnger, Gray and Christmas, partially due to

DOGE job cuts. US GDP also contracted by 0.3% last quarter driven by companies

pulling forward imports to avoid Trump’s tariffs and an increase in gold

trading activity. Businesses are increasingly pressing

·

On 03/05,

economist see a darkening outlook for the US economy but are sticking by

projections for 2 interest rate cuts from the Fed. ¾ of them surveyed by

Bloomberg predict a recession or a zero-growth scenario that narrowly avoids a

recession in the next 12M up from 26% in March. Median estimates still saw the

Fed cutting only by 25 bps in Sep and Dec 2025. Fed officials have so far left

interest rates unchanged YTD.

·

For equities, the

relief rally due to Trump’s back pedalling has caused SPX and MSCI World to

surge 3.5% and 5.4% in a matter of weeks. Key benefiary of this sentiment boost

has been MSCI Europe and MSCI Asia ex-Japan which gained 8.5% and 12%

respectively. China A-Shares been resilient but only gained 0.9% - 1.5%.

Interestingly, HSI and HSCEI surged by 9% and 7.6% demonstrating that foreign

capital have come into those market to play the China story this time round. In

particular, the HSI is trading well within the existing congestion channel. Indian

equities also done well with SENSEX and Nifty both +9.2% and +9.4%

respectively. Sector-wise moemntum

stocks are in favor with MTUM +8.1% which makes total sense.

·

Volatility

indices unsuprisingly have all dropped 15.4 – 35.4% due to the same relief

rally except for OVX which gained 16.1%. Upon closer inspection, oil prices

been on the downtrend since Ukraine War 2022 which explains the vol spike.

Fixed income markets havent been seeing much action given rate pause by the Fed

earlier. REITs are all in positive territory gaining 1 – 8.6% with AXSR and IYR

being the clear outperformers. AXSR actually continues the long-term flag

breakout pattern which happened as far back as 2020.

·

US officials are

now exploring ways of challenging the tax-exempt status of non-profit

organisations headed by new IRS lawyer Andrew De Mello. Trump also said he

would revoke Harvard University tax-exempt status as part of his wider attack

on elite universities he deems left-wing and anti-American.

·

On 02/05, Trump’s

de minimis exemption expired and the 145% tariff went into immediate effect onn

all products ordered directly from China-based retailers. Almost 1B low-cost

packages worth more than $66B were imported to the US in 2023 and 67.4% were from

China. Shein, Temu and Amazon and plenty of smallewr firms reply on imports and

build their business models about the de minimis exemption. Last month, Shen

and Temu started hiking prices which wont help Trump’s approval rating which is

down to less than 42% in part due to concerns about the direct of the economy

and impact of tariffs. Trump had labelled the de minimis exemption a “big scam”

adding “were putting an end to it”.

·

On 03/05, US

Secretary of Commerce Howard Lutnick says factory gigs are the “great jobs of

the future” that Gen Z could work in for the rest of their life and so could

their grandkids. Whilst Lutnick says this is all part of Trump’s larger planb

to make America more independent from foreign imports and services, the

adminstration targeted deportation of immigrants has left many domestic

manufacturers scrambling for labor. To keep up with supply, people have to fill

the plant jobs and Lutnicks technicians tending to the factory robots are the

next hot gig.

·

On 23/04, Trumps

softened his tone again on China saying he will be “very nice” in negotiations

with Beijing in hopes of securing a trade deal. Trump also insisted that XJP

called him despite Beijing’s denial and said “I don’t think that a sign of

weakness on XJP behalf”. He also back-tracked his threats to fire Fed Chair

Powell but added he would like him to be “a little more active” on cutting

interest rates. This comes after calling Powell a major loser whose

“termination cannot come soon enough”.

·

On 03/05, Warren

Buffet sounded the alam on the USD warning that America’s fiscal recklessness

could erode the value of it own currency. He noted that government behaviour

increasingly seemed designed to weaken the dollar, not protect it. And whlist

he acknowledged the dollar remained dominant globally, he made it clear he is

looking elsewhere – point to Berkshire’s increased exposure to JPY as a

strategic move. This rare warning comes at a time that Berkshire been selling

stocks for 10 straight quarters, dumping $134B in 2024 including trimming its

massive Apple and BofA shares. The company’s cash pile now stands at $347B

which is a record high, signalling Buffett is bracing for macroeconomic

turbulence.

·

On 30/04, Mark

Mobius said that he is keeping the bulk of his funds’ holdings in cash as he

waits out the trade-related uncertainty which is likely to persist for up to

6M. “At this stage, cash is king. So 95% of my money in the funds are in cash”

said by Mobius in an interview on Bloomberg TV. He also added that he will not

hold so much cash for more than 3 – 4M and start to deploy some of the funds

depending on where the opportunities are.

·

On 29/04, Trump

is tipped to partially ease the effect of his tariffs on autos, bocking duties

on cars made overseas from stacking on top of broader levies he has imposed.

WSJ also added that some tariffs on froeign parts used to manufacture cars in

the US will be relaxed as well. This moves will mean autos will not need to pay

higher tariffs for items like steel and alumnium nothing that carmakers will

also be able to ask for reimbursement for any tariffs they have already paid.

Automakers were able to secure these actions by committing to help advance

Trump’s goal of promoting domestic manufacturing

·

On 28/04, markets

were rattled when US Treasury Secretary Scott Bessent said it “was up to China

to de-escalate” tariffs and there are growing worries that unless there is a

breakthrough, permanent damage will be wrought on supply chains. China has

moved to make some exemptions but has held off stimulus, betting Washington

blinks first. Peter Navarro is the hardline pro-tariff advocate on one side

whilst Bessent and Lutnick are pro-free trade. Apparently, Beesent and Lutnick

pleaded with Trump to paus the reciprocal tariffs as the bond market was

starting to falter.

·

On 27/04, Scott

Bessent also ednied US-China tariffs talks despite Trump claims. Trump has in

recent weeks showed some openness to a deescalation in trade tensions with

China, amid growing concerns over the eocnomic impact of a trade war. Trump

also signalled that tariffs against China could come down althrough this would

require Beijing to come to the negotiating table.

·

The thesis that

the US govt could live off tariff revenue is a big stretch as in 2024, about

50% of all US federal revenue came from individual income taxes and whilst

tariff revenue has been pouring into the Treasury at a record amount in 04/25,

the revenue may not even be enough to p;ay for the extensions of the Tax Cuts

and Jobs Act, let along anything else. SCB strategist Steven Englander said

that whilst US collected custom duties $15B in the first 16 business days of

April which is +130% from 2024, the increase in tariff revenue is likely tot

total a little less than 0.4% of GDP over a fully year. Also, whilst tariffs

are lifting government revenue they could also trigger inflation.

·

A theory emerging

is that the cross-messaging and chaotic nature of the Trump’s tariff rollout

could be part of a carefully executed game theory. Bessent is calling it

“strategic uncertainty” and that Trump has shown the stick via high tariffs and

the carrot is the opponent taking off their tariffs and non-tariff trader

barriers.

·

On 28/04, there

was a rally earlier driven de-escalation of the trade war with China,

Trump/Powell feud and rising anticipation for the announcemnt of numerous

treade deals and solid Q1 earnings according to the Stevens Report. The

strategist also pointed out that tension between Trump and Fed Chair Jerome

Powell are far from resolved. Trump understands that firing Powell would hammer

markets so he probably wont try it but that doesn’t mean negative headlines are

done. Looking ahead, its is very unlikely that the 2025 S&P 500 EPS

expectations stay at $270 and reduction to $260 seem appropriate.

·

On 28/04, JPM

strategist Mislav Matejka maintain a cautious stance amid elevated macro risks,

softening data and continued trade policy uncertainty. Stosk may become more

attractive to buy in the 2H25 as despite soft economic indicators such as

consumer sentiment, future output expectations and labor market perceptions

deteriorating, hard data like industrial production and job gains remain

resilient. Regionally, Matejka believes international markets currently offer a

better risk-reward profile than the US without the potential to outperform in

both recessionary and recovery scenarios.

·

Commodities

havent really moved much with SPGCSI -0.3% last few weeks which is unsurprising

given the oil futures representing the commodity futures with the highest

trading volume continue to trade weak. Only XAU/$ and XAG/% have gained 7% and

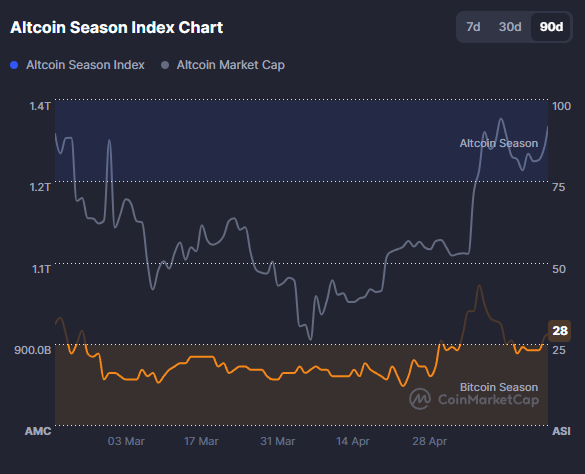

5.2% respectively. Crypto currencies also lacklustre with BTC/$ still stuck

below $100 handle. Even DOGE/$ only gained 8.8% which is tiny by crypto

standards.

·

On 04/05, oil

prices declined but pared back earlier losses after OPEC+ group singal it will

further increase production in the coming months by 411k barrels per day. The

increase is nearly 3x the volume initially signaled with key contributors KSA

and Russia. Barclays analyst have lowered their Brent forecast to $66/bbl for

2025 and $60/bbl for 2026 on the back of this development.

·

On 28/04, JPM has

reaffirmed it bullish stance on EMEA gold mining sector, forecasting as much as

60 – 90% upside if gold prices reach $4000 per ounce by mid-2026. The bank also

emphasized the macro backdrop namely stagflation risk, recession fears and

global policy uncertainty continue to support strong institutional and retail

gold demand. They also added that

“increased probabilities and potential for quicker Fed cuts in response further

reinforce this bullish narrative”